Unless you’ve already arranged for a job in Israel or are continuing to work at your old job, estimating your income is very difficult to do. Israeli taxes need to be calculated to know what your net (netto) monthly salary will be. There are many online calculators that can help with this estimate.

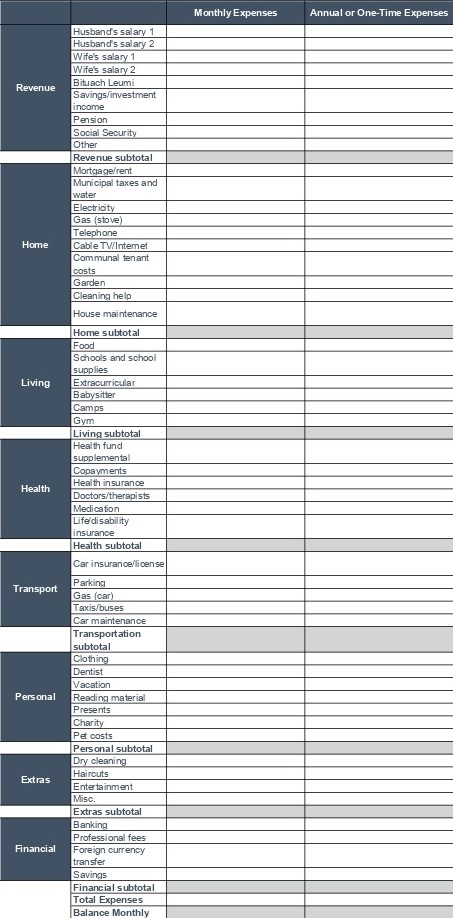

Start by completing the following table. Include all sources of income, including government and organizational subsidies. Monthly stipends like rental subsidies go into the first column, and lump-sum payments go into the second column under annual revenue. Include income from Bituach Leumi (child care allowance and any projected additional payments), from family abroad, and income derived from any investments or pensions. If you don’t have exact numbers, estimate conservatively as you can always refine the numbers as you get closer to Aliyah, or after your arrival.

Bituach Leumi offers a monthly child allowance per child under the age of eighteen. The sums for those born after June 1, 2003 (as of 2020) are NIS 152 for one child, NIS 338 for two children, NIS 526 for three children and then NIS 150 for each additional child, or NIS 284 for children born before that date).

In January 2017 Bituach Leumi initiated a savings scheme for every child under the age of 18. Under the scheme every child receives NIS50 per month from Bituach Leumi which goes into a savings fund of the parents’ choosing. (Parents also have the option of adding an additional NIS 50 per month from their Bituach Leumi child benefit allowance to boost the savings fund.) The aim of this scheme is to ensure that every child has a savings account in his/her name.

Unemployment benefits only begin after your sal klitah (absorption basket allowance) is finished, if you’re not a student in any educational framework, and if your spouse is not employed. Where the head of the household is under 55, a single oleh is entitled to NIS 1,524 per month, a couple NIS 2,179, and a couple plus one child gets NIS 2,491, with the maximum that a family can receive being NIS 2,839. This allowance is only provided in the first year of Aliyah. After that time, contact Bituach Leumi to see if you qualify for income support, or havtachat hachnasah.

It’s important to estimate your monthly income conservatively. According to the Israeli Central Bureau of Statistics the average gross salary for 2020 across the entire economy is only NIS 12,876 a month. While this may be slightly low, it still offers perspective. The average family in Israel (of two adults and two children) spends approximately NIS 12,000–13,000 a month (the average for Anglos is significantly higher) — that’s total net income per family (after taxes), based on multiple salaries.

Research comparable salary levels in the fields you are considering and then take the low end of the range of salaries quoted — even those with extensive experience usually take large pay cuts when they arrive. It’s not unusual to receive a starting salary that’s only a fraction of what you earned abroad. Don’t be discouraged — salaries can grow substantially, and can also contain many benefits (see “Understanding the Israeli Employment Market”). Many employers are reluctant to pay high salaries for someone they don’t yet know — but the more experience you develop in Israel, the more possible it will be to attain a higher salary.

A self-employed person often does not know what his monthly income will be. Talk to others in your field to get an idea, but remember that it might take years to get to that level. Average out your expected monthly income, taking into account that there are always high and low seasons for almost every business. Put aside money during the good months to save for the bad months. Once you arrive, track your revenue and expenses monthly to determine where they are coming from and whether they are seasonal. If you know which times of year are likely to be busy and which are likely to be slow, plan vacations during the slow times. Also, plan your marketing and other essential business activities during the low points as opposed to the high, when there is little spare time.

Ensure that you are maximizing your income given the Israeli tax system. For example, if your income is currently being earned by one spouse, find out if there is a legal way to split it between spouses in order to take advantage of the Israeli tax code. When negotiating your salary, ensure that you’re getting all the standard benefits such as pension contributions and advanced savings plans (keren hishtalmut), as these elements play a big part of your long-term financial success in Israel.

The size of your home will go a long way towards shaping your overall budget. It will impact not only the mortgage or rent, but also municipal taxes, property and mortgage insurance, water, electricity, gas, shared building costs, cleaning expenses, household supplies, and maintenance. Think carefully about where you want to start off living in Israel and research the market online — prices can vary tremendously between cities in Israel. While an extra room or a garden might not seem substantial, the effect on all other home expenses can be major.

Estimate all the associated costs of your new home. The three sample budgets in the section “Starting your financial plan” are meant to give you a point of reference only. Your budget must be personalized to reflect your individualized circumstances.

Municipalities offer discounts to olim for one year during their first two years in Israel. Include projected discounts from municipalities in your budget. Estimate any renovation cost before or during your initial period in your home — even if you’re only renting. These expenses should be included in the second column, along with your annual or one-time expenses. Don’t forget that the do-it-yourself approach is also a viable and common option — there are endless websites and tips for the DIY amateur.

If you have the time and patience to learn new skills, you can fix up your home, save yourself a great deal of money, and perhaps discover some latent talents.

Utility prices are high in Israel, with electricity and water prices significantly more expensive than abroad. Don’t use these resources the same way you did back home, or you might be shocked at the size of your bills. For example, if you’re used to running your air-conditioning 24/7, you can expect to find yourself with an electrical bill of thousands of shekels a month. If you can’t afford that large an expense, change your energy consumption habits. There are many ways that you can save on your usage, from using timers to fixing leaks. Furthermore, ensure you’re receiving all the discounts you’re entitled to as an oleh.

Phone expenses can be a major drain on your budget. Don’t be overwhelmed by your phone costs. Budget in advance how much you can afford and stick to it by buying minutes or limiting family usage. International VOIP lines can save you money if you make many international calls, but ensure they’re truly worth it, as long distance charges are only agorot per minute. The last few years have brought a very welcome decrease in communication costs and the ability to change providers easily. Take advantage of this situation. Shop around and see which companies offer you the best deals for your needs (if you need more than one phone account, there are often preferential rates). And don’t forget to reassess your rates every year (if not more often) as you will be able to renegotiate your terms.

Living costs include a range of expenses that vary tremendously among different families. They include food, education (both regular tuition and extracurricular activities), private lessons, babysitting, and clothing expenses. The average Israeli family spends significantly less on these areas than the average oleh family.

The top ten percent of Israeli earners spends on average approximately NIS 2,500 a month on food, while the lowest ten percent spends only NIS 1,500. The overall average is less than NIS 2,000 a month for a family of four. Most oleh families spend significantly more than this, sometimes causing serious financial trouble. Under ordinary circumstances, food expenses should not be much more than 20–25% of your monthly budget, or staying afloat financially will be difficult. Start by taking a rough estimate of NIS 600 per person per month for the first two people, and then add an additional NIS 500 per person, and you’ll get an estimate of what you can expect to spend (taking into account the economies of scale that the more family members you have, the per-person costs should go down).

There are many ways to reduce your food bill. Doing an online search will reveal an almost endless number of hints and suggestions that can help. The most significant way to stay within your budget is to have a clearly defined sum that you can afford to spend each month (this concept applies to budgeting other expense items as well). Clearly defining what you can spend allows you to create a plan to keep within the budget framework. If you can afford to spend NIS 3,000 a month on food, break down your monthly spending into 4.2 weeks of approximately NIS 700 a week. Physically withdraw exactly NIS 700 a week in cash for food, and you’ll have a good chance of staying within your budget framework (unlike shopping with a credit card and having no idea how high the bills actually are). Keep track of your food expenses to avoid a major surprise.

Here are a few other ideas to help you save money when shopping:

Plan your weekly menu in advance.

Shop around — price differentials can be significant even between the larger supermarkets chains. Know what’s cheaper where.

Don’t shop for fun or as a family activity.

The fewer times you enter a store, the less you’ll spend.

Bulk shopping can save you money, but not if you end up eating twice as much!

Avoid shopping at your local makolet (convenience store), as prices can be 20–50% higher.

While tuition expenses in Israel should be much cheaper than your average private tuition costs abroad, education in Israel is not necessarily free. If your children attend a national, national religious school (dati or mamlachti dati school), or standard Bais Yaakov or cheder, you’ll most likely only need to pay a few hundred shekels (or less) per month for each child. There are also many private schools in Israel, and their tuition fees can be substantially higher.

High schools tend to be much more expensive than elementary schools, especially those where students dorm throughout the week (a very common occurrence in Israel). So while Israeli tuition rates may never rival the incredible sums abroad, as a percentage of take-home pay, they can still comprise a significant portion of monthly expenses. Schools in Israel will often grant discounts to olim and families with multiple children attending the school. Negotiate with the school as necessary to get additional discounts. It never hurts to ask.

Clothing costs in Israel are comparable (and often even more expensive) than in many countries around the world. On the other hand, there are second-hand clothing stores (gemachim) selling top-notch new or slightly worn clothing at a fraction of the regular cost. If you’re on a tight budget, this is an easy way to cut down on monthly expenses, especially if you have the time to look around. Of course, swapping with friends and family continues to be an excellent option as well.

In general, health-related expenses in Israel are contained. Israel’s socialized medical system covers most expenses related to ongoing standard medical care. Co-payments from members are required for visits to specialists and for prescription drugs, but these payments are limited on a quarterly basis per family. All Israeli citizens are entitled to join one of four health funds that cover all basic medical services. The health funds all offer supplementary insurance covering a variety of goods and services beyond the standard coverage (each fund’s supplementary plans are different and change often).

Unless one encounters major medical issues, supplementary health coverage should amount to a few hundred shekels a month per family. When putting your budget together, consider all possible additional medical expenses, therapies, medications that are not covered in the basket of approved medicines, special treatments, and even special transportation to medical practitioners, if applicable. If a medicine isn’t covered in the basket of medicines approved by the Ministry of Health, research the cost of paying it privately and alternatives that might be on the approved list.

Beyond the medical coverage offered by the health funds, private medical insurance is also available and gives you the flexibility to treat future medical issues anywhere in the world, for as little as a few hundred shekels a month. Life insurance, see the section on insurance, is often included in your retirement pension plan, so no additional expense may be relevant — unless you continue to pay an older policy from your former country.

Unlike the average American family, the average Israeli family does not own two cars.

Even owning one car is expensive, and while owning one has become more of the norm in Israel, it’s often not an easy decision and it can weigh heavily on your monthly budget. A car’s monthly expense can vary significantly, depending on how old the car is, how far you drive, and the car’s condition. On average, a car will cost you between NIS 1,500 and NIS 2,000 a month to run and insure (not including the depreciation of the actual asset, which can add an additional NIS 500–1,000 a month to the actual operating expenses).

For the average Israeli family earning NIS 11,000 net a month, maintaining a car is a major expense that needs to be contemplated carefully. For people who don’t travel regularly outside their city, public transportation (especially in the larger cities with extensive bus and train routes), including taxis and the occasional car rental, can be much cheaper than owning your own car.

While financial charges should not initially occupy a large part of your monthly expenses, you should still expect to pay several hundred shekels a month in fees, especially if you’re bringing money into Israel and converting it to shekels every month. These fees include the standard banking fees, which range from NIS 30–80 a month, to currency conversion and transfer fees when converting from foreign currencies to shekels. Understanding how the Israeli banking system works will go a long way to ensuring that you keep down your expenses. Bank online and bargain whenever possible!

Insurance expenses can add significantly to your total budget. It might not be economically feasible (or necessary) to keep the same amount of coverage you had abroad. Determine which types of insurance you consider essential and speak to agents in Israel to get an idea of the total costs. Home property insurance will generally add NIS 100– 200 a month; additional health insurance can add several hundred extra shekels to your budget, while long-term care insurance depends greatly on your age. Look to increase deductibles whenever possible to reduce your premiums. If you have student loans or credit card debt abroad that you need to continue paying, build it into your budget. If necessary, look to restructure or refinance your debt prior to making Aliyah to reduce your monthly payments.

While you can plan for the majority of your expenses, what can you do about unexpected expenses? Set aside 8–10% of your monthly budget towards these ever-present surprises. There’s no way to anticipate everything, so build this buffer into your budget and then when the surprises arrive, at least you’ll be able to manage them.

The excitement of the move and the incredible highs of living in Israel will eventually need to be tempered by the reality that you need to be able to afford to live here, so live within your means. Setting up a budget will help you plan for the move and manage your resources through the initial integration phase. Always remember that if you do get into trouble, whether it’s with the banks, Bituach Leumi, or the courts, burying your head in the sand won’t solve your problems. Address the issues before they spiral out of control and force you to leave the country. There are unfortunately too many examples to cite which ended in ruin.

Define the goals that will deem your Aliyah a success and set them down in writing.

Recognize the difference between needs and wants.

Build a budget — and keep to it.

There are small and huge savings that can be made by those who are aware. Look around and benefit from them.

Our newsletter goes out approximately once a month, and will keep you informed of changes in the financial and other related markets that might impact you.